- English

- Español

- Português

- русский

- Français

- 日本語

- Deutsch

- tiếng Việt

- Italiano

- Nederlands

- ภาษาไทย

- Polski

- 한국어

- Svenska

- magyar

- Malay

- বাংলা ভাষার

- Dansk

- Suomi

- हिन्दी

- Pilipino

- Türkçe

- Gaeilge

- العربية

- Indonesia

- Norsk

- تمل

- český

- ελληνικά

- український

- Javanese

- فارسی

- தமிழ்

- తెలుగు

- नेपाली

- Burmese

- български

- ລາວ

- Latine

- Қазақша

- Euskal

- Azərbaycan

- Slovenský jazyk

- Македонски

- Lietuvos

- Eesti Keel

- Română

- Slovenski

- मराठी

- Srpski језик

Small & Medium-Sized Display Industry 2026: Five Growth Tracks Behind Rising Shipments and Falling Revenue

The Big Picture: Shipments Rising, Revenue Falling

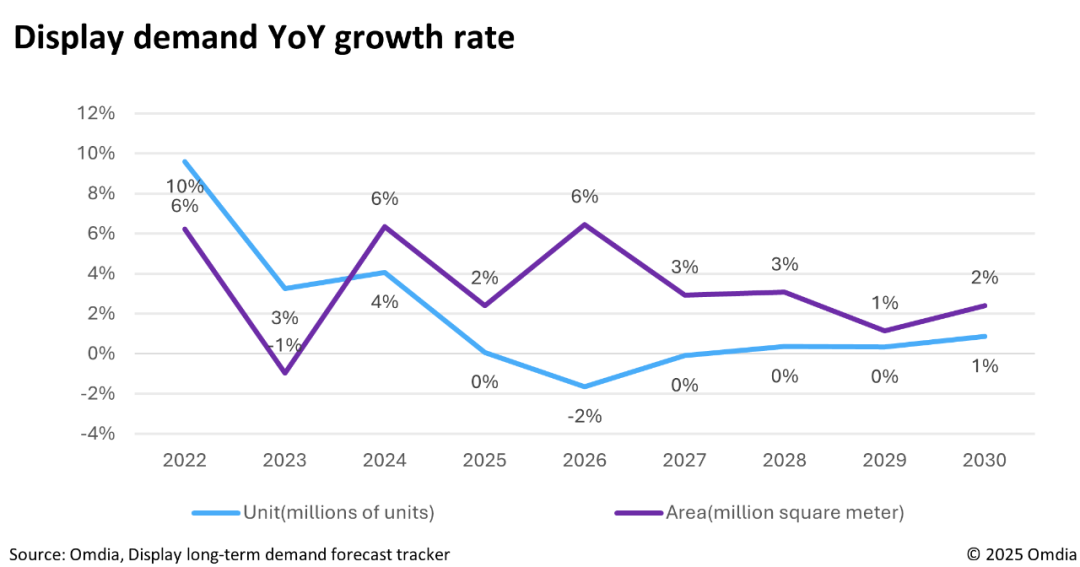

Omdia's latest June data reveals that global LED video display shipments in Q1 2026 edged up 0.6% year-on-year, yet revenue declined 2.3%—the first revenue contraction since 2022. Another signal warrants attention: Omdia projects global display panel demand to fall 6% year-on-year in 2026, with area demand growth of just 1%.

However, “rising volume, falling price” does not mean the industry lacks opportunity. Structural divergence is underway: revenue from the traditional mainstream product line (1.0–1.99mm pixel pitch) dropped 6.8% year-on-year, while demand in automotive, energy storage, and medical segments is accelerating. The ebb and flow are clear for those who look closely.

Five Tracks Worth Watching1. Automotive Displays: The Most Certain Growth Driver

Global automotive display panel shipments reached approximately 240 million units in 2025, up 4.0% year-on-year, and are projected to exceed 250 million units in 2026. The average number of displays per vehicle is climbing from 2.5 toward 3—center consoles, instrument clusters, co-pilot screens, and electronic rearview mirrors each represent an incremental module demand. Automotive OLED is growing even faster: the market expanded 56.7% year-on-year in 2025, with Omdia projecting 64.3% growth in 2026, though LCD remains dominant for mainstream applications and OLED is currently concentrated in premium models. On the technology front, Mini LED automotive displays are emerging as a new focal point—Honghe Technology debuted a 0 OD Mini LED automotive screen in June, and multiple manufacturers are pivoting from commercial display into the automotive segment.

2. Energy Storage &; Power Supply Displays: Riding the New Energy Wave

Global energy storage cell shipments surged to 612.39 GWh in 2025, a staggering 94.59% year-on-year increase, with 740 GWh projected for 2026. From January to May 2026, China's cumulative energy storage battery sales reached 255.5 GWh, up 87.7% year-on-year—2.5 times the growth rate of power batteries in the same period. Charging stations, UPS systems, and portable energy storage devices all require status display modules, with hard requirements for wide operating temperature ranges, electromagnetic interference resistance, and outdoor high-brightness performance.

3. Medical Device Displays: High Margins, High Barriers

China's medical device market reached RMB 1.22 trillion in 2025, growing at an annual average of 9.9% during the 14th Five-Year Plan period. Demand for display modules in ventilators, oxygen concentrators, and ultrasound diagnostic equipment continues to grow steadily. Once a supplier enters the medical device supply chain, switching costs are high and customer stickiness is strong. Medical-grade certification, wide operating temperature support, and long-lifecycle supply commitments are the barriers to entry.

4. HMI (Human-Machine Interface): From Selling Screens to Selling Solutions

Customers no longer need just a screen—they need an integrated “display + touch + control” solution. Touch-display integration, customized dimensions and interfaces, and application-specific control schemes signal that module manufacturers' value is migrating from hardware to solutions. The player who can deliver a plug-and-play interactive solution captures the higher margin.

5. Small &; Medium-Sized OLED: IT and Automotive Are the Real Growth

Smartphone AMOLED penetration has plateaued (projected at 43.2% in 2026, up just 2 percentage points from 2025), but IT OLED is surging: OLED laptop shipments are projected to grow 44.9% year-on-year in 2026, and OLED desktop monitors by 58.0%. BOE's 8.6th-generation OLED production line officially began mass production on June 17, marking an inflection point for medium-sized OLED commercialization. RUNTO forecasts that OLED panel prices for laptops will decline by more than 30% by the end of 2027. For module manufacturers, automotive OLED and industrial OLED are segments worth positioning for early.

Two Risks to Monitor

First, global panel demand is being revised downward across the board. Middle East geopolitical tensions and rising memory costs are pushing PC brands to raise prices by 20–30%, which may further suppress end-market demand. Second, the price war shows no signs of ending soon. Revenue from 1.0–1.99mm pixel pitch products continues to slide, and under the “rising volume, falling price” paradigm, competing on price alone is an increasingly narrow path.

Conclusion: The industry faces overall headwinds, but automotive, energy storage, and medical displays offer high-demand certainty. HMI solution capabilities and differentiated OLED positioning are the keys to profitability. Rather than competing on price in a red ocean, the winning move is to go deep and narrow in the right segments.

About CNK

Founded in Shenzhen in 2010, CNK Electronics (CNK in brief) expanded the world leading factory in Longyan, Fujian in 2019. It is a national specialized and innovative "little giant" enterprise that specializes in the design, development, production and sales of display products. CNK provides customers with a full range of cost-effective small and medium-sized display modules, solutions, and services with excellent quality worldwide. Oriented in technology and high quality, CNK keeps sustainable development, works to offer customers better and stable services.